(English follows Spanish)

(English follows Spanish)

por MEDA Intern Jack Wilger

Traducción por Lucia Obregon

A fines de diciembre del 2017, el gobierno federal aprobó la “Ley de Reducción de Impuestos y Empleos.”

El objetivo principal de la nueva ley es la reducción de los recortes tributarios corporativos, sus cambios en el código tributario también afectarán la manera en que la mayoría de nosotros presentamos los impuestos en los próximos años. Todos estos cambios van a estar en vigencia tras 2025; después, pueden renovarse, vencerse o modificarse de alguna manera.

Los cambios de la nueva ley para individuos y familias se centran en cuatro elementos:

- Categorias de Ingreso

- Deducción Estándar y las Exención Personal y de dependientes

- Crédito Tributario por Hijo (para familias con niños menores de 17 años)

- Mandato Individual (Ley de Cuidado de Salud Asequible)

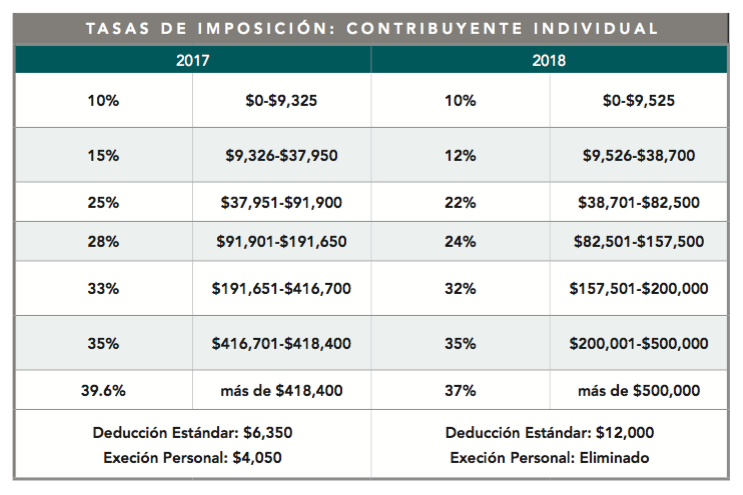

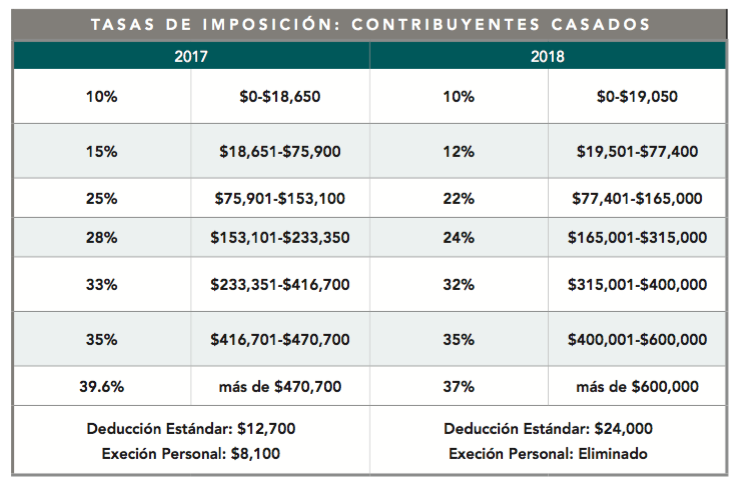

1. Categorias de Ingreso

Una forma en que la nueva ley afectará a muchos clientes de MEDA son los cambios en las tasas de imposición o nivel de ingreso. Estas tasas determinan el porcentaje imponible de cada porción de un contribuyente o el ingreso conjunto de los contribuyentes casados.

Los cambios en cada categoría son los siguientes:

La cantidad de ingresos en cada categoría, excepto en la categoría más baja, disminuye varios puntos de porcentaje. Esto podría ayudar a los clientes de MEDA que tienen un ingreso bajo para obtener una devolución de dinero más significativo.

2. Deducción Estándar y las Exención Personal y de dependientes

El mayor cambio de la nueva ley para muchos clientes parece ser los cambios a la deducción estándar. Todos los contribuyentes van a tener que elegir anualmente entre tomar la deducción estándar (siempre una cantidad fija en dólares) o deducciones detalladas (preferible si tales deducciones son mayores que la deducción estándar). Ambas deducciones permiten a los contribuyentes exentar de imposición una parte de sus ingresos.

La mayoría de los clientes de MEDA eligen la deducción estándar y las nuevas limitaciones en las deducciones detalladas no son motivo de gran preocupación para muchas personas.

La deducción estándar casi se ha duplicado:

- Antes de 2018: $ 6,500 por persona declarando como soltero/a; $ 13,000 por pareja casada declarando juntamente

- En el 2018: $ 12,000 por persona declarando como soltero/a; $ 24,000 por pareja casada declarando juntamente

Desafortunadamente, esta ganancia significativa se compensa con la eliminación de la exención personal.

Anteriormente, los contribuyentes podían recibir una exención por cada contribuyente y dependiente que reclamaban ($ 4,050 por persona en 2017) si elegían la deducción estándar.

Aunque la deducción estándar excede la anterior para un solo contribuyente o una pareja, con múltiples dependientes la devolución comienza a disminuir en valor. Este cambio penalizará a las familias que reclaman a varios hijos al declarar impuestos. El resultado puede ser desincentivar que los clientes con dependientes que viven en el extranjero reclamen números de ITIN para esos familiares.

3. Crédito Tributario por Hijo (“Child Tax Credit”)

Los clientes elegibles para el Crédito Tributario por Hijo (para familias con hijos menores de 17 años) también se verán impactados por la nueva ley.

Los cambios en el Crédito Tributario por Hijo son los siguientes:

- El crédito máximo recibido por niño se duplica de $ 1,000 a $ 2,000.

- La versión reembolsable del crédito, antes $1,000 por hijo, será $ 1,400 por hijo.

- Los niños deben tener un Número de Seguro Social para ser reclamado; anteriormente, los niños con ITIN también calificaban.

Los primeros dos de estos cambios pueden beneficiar mucho a los clientes de MEDA. El incremento del crédito puede ser sustancial, y el crédito reembolsable significa que los clientes cuyos créditos exceden su responsabilidad fiscal pueden recibir hasta $1,400 de regreso. Antes de esta ley, este crédito se perdería.

Por el contrario, el requisito de Números de Seguro Social se impondrá. Si los dependientes NO tiene números de Seguro Social, ya no serán elegibles para el crédito. Eso significa que las familias indocumentadas con niños que viven en los estados Unidos pueden perderse hasta $3,000 al año.

4. Mandato individual (Ley de Cuidado de Salud Asequible)

Los clientes que no pueden pagar o no quieren comprar un seguro médico se beneficiarán de los cambios con esta nueva ley, aunque no hasta el año tributario de 2019. Anteriormente, bajo la regla usualmente llamada el “mandato individual,” aquellos que no tenían seguro médico tenían que pagar una multa basada en el ingreso familiar.

A partir del año tributario de 2019, la nueva ley fiscal elimina la multa del mandato individual, lo que significa que los clientes que no pueden pagar el seguro médico ya no serán penalizados. Una familia con ingreso relativamente bajo para San Francisco puede ahorrar hasta $1,400 al año.

Conclusión

La “Ley de reducción de impuestos y empleos” contiene cambios que puede beneficiar a muchos de los clientes de MEDA al declarar sus impuestos, aunque algunos de estos beneficios desaparecerán con el tiempo. Algunos clientes se verán impactados negativamente para aquellos dependientes sin Seguro Social.

Hay suficiente tiempo para que los contribuyentes se enteren de los cambios en la ley fiscal antes de presentar sus impuestos en 201

Como siempre, el equipo de MEDA está aquí para responder sus preguntas. Póngase en contacto con nosotros al (415) 282-334 ext 178 con cualquier pregunta o inquietud que pueda tener sobre los cambios en la ley de impuestos.

_____________________________

How Will the New U.S. Tax Law Affect Your Family’s Financial Health?

by MEDA Intern Jack Wilger

Translation by Lucia Obregon

In late December 2017, the federal government passed the “Tax Cuts and Jobs Act.”

While the new law’s main focus was on the reduction of corporate tax cuts, its changes to the tax code will also impact the way most of us file taxes in upcoming years. All of these changes are in effect through 2025; after that they may be renewed, allowed to expire, or modified in some way.

The new law’s changes for individuals and families center around four items:

- Tax brackets

- Standard deductions, personal exemptions and dependent exemptions

- Child Tax Credit

- Individual mandate (Affordable Care Act)

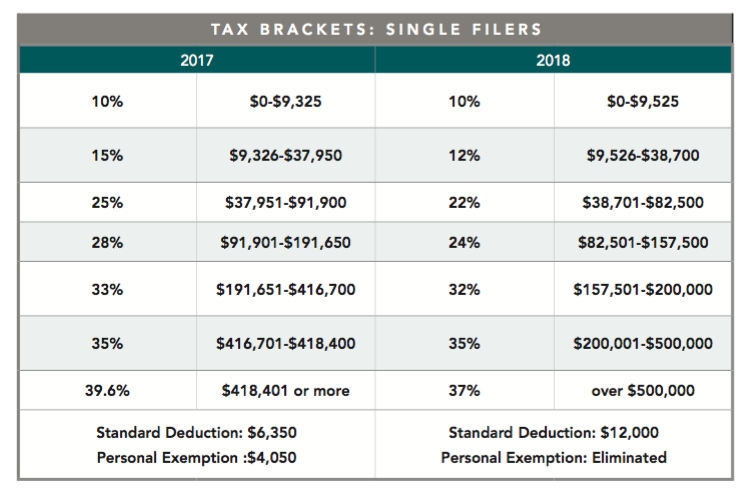

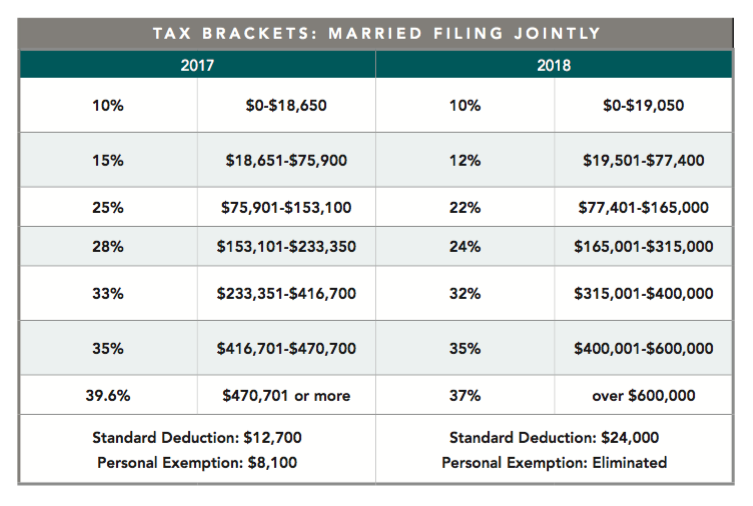

1. Tax brackets

One way the new law will impact many MEDA clients is changes to the income tax brackets, which determine the taxable percent of each portion of a single filer or jointly filing married taxpayers’ income.

The changes to each tax bracket are as follows:

The amount of income taxed in every bracket — except for the lowest bracket — falls by several percentage points. This could potentially save MEDA clients, other than the extremely low-income, a modest amount of money.

2. Standard deductions, personal exemptions and dependent exemptions

The new tax law’s largest effect on many clients looks to be the changes to the standard deduction. All taxpayers must annually choose between taking the standard deduction (always a fixed dollar amount that depends on your filing status) or itemized deductions (preferable if such deductions are greater than the standard deduction). Both deductions allow taxpayers to remove portions of their income from taxation.

Because the majority of MEDA clients choose the standard deduction and are lower-income, the new limitations on itemized deductions are not of great concern for many people.

The standard deduction has been nearly doubled:

- Prior to 2018: $6,500 for a single filer; $13,000 for a married couple filing jointly

- 2018: $12,000 for a single filer; $24,000 for a married couple filing jointly

Unfortunately, this significant gain is somewhat offset by the elimination of the personal and dependent exemption.

Previously, taxpayers could receive an exemption (that is, an amount of their income to be treated as tax-free) for every taxpayer and dependent they claimed ($4,050 per person in 2017) if they chose the standard deduction.

While the new standard deduction value exceeds the old one plus the personal exemption for a single taxpayer or a couple, with multiple dependents the new law begins to be less advantageous for taxpayers. This change will penalize families with multiple children who claim several dependents when filing taxes, and disincentivize clients with dependents living in Mexico or Canada from applying for Individual Taxpayer Identification Numbers (ITINs).

3. Child Tax Credit

Clients eligible for the Child Tax Credit, which reduces taxes for families with children, will also be affected by the new tax law.

The changes to the Child Tax Credit are as follows:

- The maximum possible credit per child doubles from $1,000 to $2,000.

- The refundable version of the credit now goes up to $1,400; previously, it maxed out at $1,000.

- Children must have a Social Security Number to be claimed; previously, children with ITINs qualified for the credit.

The first two of these changes may greatly benefit MEDA clients. The increase in the credit amount may be substantial, and the refundable credit means that those whose tax credits exceed their tax liability may receive up to $1,400 back, whereas previously the credit was lost.

In contrast, the requirement of Social Security Numbers means that children of undocumented immigrants, who are not able to obtain Social Security Numbers, will no longer be eligible for the refundable version of the tax credit. That means some families with undocumented children in their U.S. households will lose as much as $3,000 a year in tax credits.

4. Individual mandate (Affordable Care Act)

Clients who cannot afford to or do not want to buy medical insurance will benefit from the changes to the tax code, although not until tax year 2019. Previously, under a rule often called the “individual mandate,” those who did not purchase medical insurance had to pay a fine which came as either a per-person fee or a percentage of household income.

Starting with 2019, the new tax law eliminates the individual mandate’s fine, which means that clients who could not afford to pay for medical insurance will no longer be penalized. Households that were relatively low-income by San Francisco standards may save as much as $1,400 a year in fines.

Conclusion

The “Tax Cuts and Jobs Act” contains changes that will positively impact the way MEDA clients file their taxes, although some of these benefits will go away over time. There are also some negative impacts for certain clients.

There is plenty of time for taxpayers to learn of the changes to the tax law before they file their taxes in 2019 — for the 2018 calendar year — so that they may adjust their spending habits as needed.

As always, the MEDA team is here to answer your questions. Contact us at (415) 282-334 ext 178 with any questions or concerns you may have around changes to the U.S. tax code.

Leave a reply